We no longer support this browser. Using a supported browser will provide a better experience.

发现

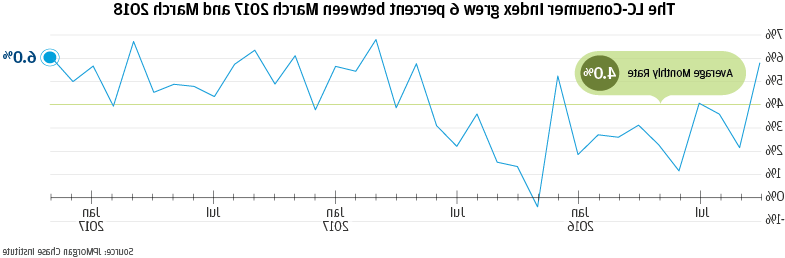

- 去找1Between April 2015 and March 2018, the LC-Consumer Index averaged 4 percent in year-over-year growth.

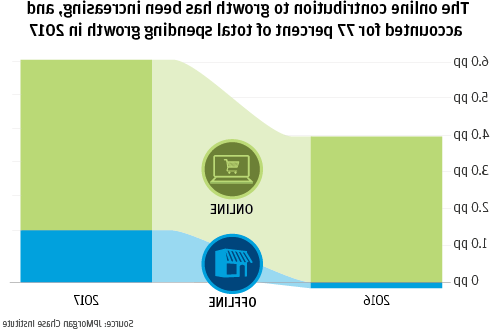

- 去找2Online spending has driven overall growth in the LC-Consumer Index, at times almost exclusively.

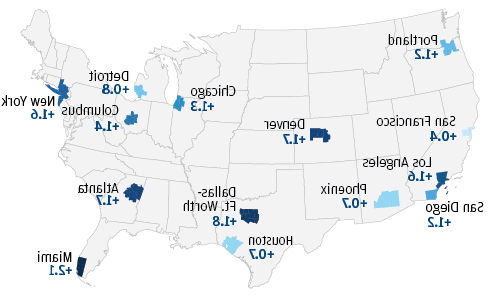

- 去找3Non-local shares of LC-Consumer spending are increasing in every metro we track.

- 去找4Online commerce growth is driven by contributions from non-local merchants.

- 去找5Online spending growth is driven by high-income consumers between the ages of 35 and 54.

下载

2018年12月

In 2016 the metropolitan share of US Gross Domestic Product was nearly 90%. Given the large share of economic output from metropolitan areas it is critical for stakeholders, 研究人员, and policymakers to have granular, high-frequency economic measurement and analyses at the metropolitan level to complement existing local economic research.

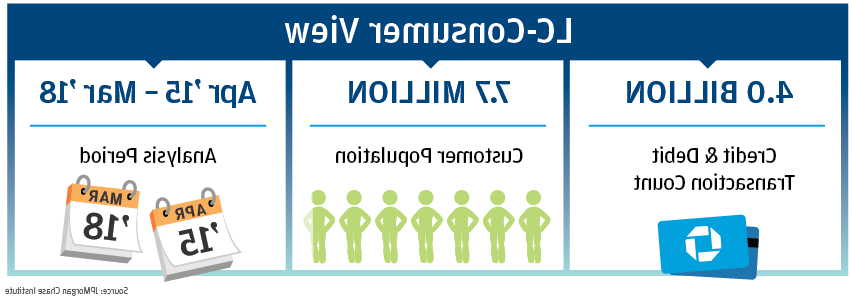

在这份报告中, the 澳博官方网站app 研究所 expands the scope of our Local Commerce (LC) analyses through the introduction of our consumer view – namely, the transactions executed by consumers residing within a given metro area. This view complements the merchant view leveraged in our existing Local Commerce Index which examines the transactions executed at merchants located within a given metro area. The consumer view enables exploration of the extent to which online commerce has affected growth, who has driven that growth, and how it has impacted the offline marketplace.

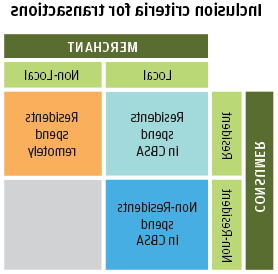

What are the Dimensions of Local Commerce?

The 澳博官方网站app 研究所 frames the Local Commerce lens along three dimensions:

- Customer Residence,

- Merchant Location, and

- Transaction Channel (online/offline)

Customer and merchant locations allow us to understand the extent to which customers are shopping at local merchants versus merchants that are located in different metro areas. The transaction channel allows us to understand whether or not the purchase was a made at a distance.

找到一个: Between April 2015 and March 2018, the LC-Consumer Index averaged 4 percent in year-over-year growth.

- Resident spending growth increased substantively throughout 2016. Growth through September 2016 averaged 2.9%, while growth after averaged 5.2%.

- Growth levels remained elevated throughout 2016 and 2017.

- Growth in spending captured by the U.S. Census Bureau’s Monthly Retail Trade Survey increases more gradually in comparison to the LC-Consumer Index.

发现二: Online spending has driven overall growth in the LC-Consumer Index, at times almost exclusively.

- The relatively high, sustained growth in resident spending has largely been driven by online commerce, which has contributed a monthly average of 4.0和4.7 percentage points (pp) in 2016 and 2017, respectively.

- The quarterly year-over-year growth of online spending in the LC-Consumer Index over the 2015 Q2 to 2018 2Q time period was 3.1 pp lower in the LC-C (11.7 percent) than in the US Census Bureau’s E-Commerce Series (14.8%).

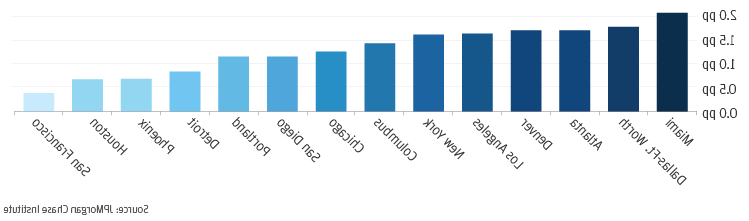

发现三: Non-local shares of LC-Consumer spending are increasing in every metro we track.

发现四: Online commerce growth is driven by contributions from non-local merchants.

- Overall spending growth is dominated by contributions from online spending at non-local merchants, 造成3.2和4.1 pp in 2016 and 2017, respectively. This is in comparison to the smaller 1.5和1.1 pp contributions from online spending at local merchants in 2016 and 2017, respectively.

- For offline transactions, spending at local merchants is the dominant driver of growth

发现五: Online spending growth is driven by high-income consumers between the ages of 35 and 54.

- Consumers under 35 across all income brackets tend to contribute strongly to online growth, but high-income 35-54 year olds are the dominant contributors to growth in the online market. This group contributed 3.3 pp to overall growth in 2017.

- The growth contributions from high-income 35-54 year olds were 94 percent higher than the next closest group (low-income consumers under 35) in 2017.

- This dominance by high-income 35-54 year olds is largely driven by the fact they hold the largest market share in online spending.

The consumer view of Local Commerce provides a granular view of online spending and its implications for local economies that is difficult to capture via other data sources. Our initial analysis has revealed that the growth rate for online spending is highest for lower income customers under 35, but the largest contributions to growth come from the high-income 35-54 year olds. High and growing shares of LC-Consumer spending take place online and this is true across all metro areas we tracked. This growth in online spending has been accompanied by an increase in spending at merchants that are located outside the metro area of the consumer. The implications of these changes for local economies are not yet clear, but the LC-Consumer Index can provide unprecedented insight into an evolving commerce landscape.